10 d’agost 2020

09 d’agost 2020

08 d’agost 2020

07 d’agost 2020

06 d’agost 2020

05 d’agost 2020

04 d’agost 2020

03 d’agost 2020

02 d’agost 2020

01 d’agost 2020

18 de juny 2020

Opioid crisis

Deaths of Despair and the Future of Capitalism

Beyond covid crisis there is still another one in US: the opioid crisis. The most relevant book on the topic is the Case-Deaton one.

Ps. Medicaments i risc de pneumònia

Els analgèsics opiacis causen depressió respiratòria amb la hipoventilació pulmonar resultant;

alguns d’ells (codeïna, morfina, fentanil i metadona) també tenen efectes immunosupressors.

Incrementen el risc de pneumònia i la mortalitat respiratòria en un 40 a 75%.26,27,28

L’any 2018, uns 50 milions de persones als EUA (15% de la població adulta, 25% entre els més

grans de 65 anys) reberen una mitjana de 3,4 prescripcions d’analgèsics opiacis, i 10 milions de

persones reconeixien consum exagerat d’analgèsics de prescripció mèdica.29 A Europa en els

últims anys el consum d’opiacis suaus y forts ha augmentat, sobretot entre la gent gran.30,31

Fentanil i morfina son els opiacis forts més consumits, i més recentment oxicodona. El

tramadol, que és també inhibidor de la recaptació de serotonina, és l’opiaci suau més consumit.

En dos estudis observacionals de publicació recent, el consum de tramadol, comparat amb el

d’AINE, es va associar a una mortalitat 1,6 a 2,6 vegades més alta,32,33 sobretot en pacients

amb infecció i en pacients amb malaltia respiratòria.

Beyond covid crisis there is still another one in US: the opioid crisis. The most relevant book on the topic is the Case-Deaton one.

We are telling the story in the way that we uncovered it, starting with midlife deaths of all kinds. We then focused on the immediate causes, which turned out to be deaths of despair among whites plus a slowdown and reversal in deaths from heart disease, which, until then, had been a main engine of mortality decline. Unfortunately, deaths of despair are not only afflicting middle-aged whites. While the elderly have been largely exempt, there have also been rapid increases in deaths of despair—particularly from overdoses and suicides—among younger whites. For whites between the ages of forty-five and fifty-four, deaths of despair tripled from 1990 to 2017. In 2017, this midlife age-group

had the highest rate of mortality from deaths of despair. But whites in younger age-groups were also doing badly and their deaths rose even more rapidly, accelerating in the last few years.

Drug overdoses are the single largest category of deaths of despair. They are part of a broader epidemic that includes death from alcoholism and suicide, a reflection of the social failures that we have described in this book. Yet the behavior of the pharmaceutical companies caused more deaths than would otherwise have happened, showering gasoline on smoldering despair. Stopping the drug epidemic will not eliminate the root causes of deaths of despair, but it will save many lives and should be an immediate priority. Addiction is extremely hard to treat, even with the cooperation of the addict. There appears to be wide agreement that medication-assisted treatment can be effective, but it is not available to everyone, often because of cost.

Ps. Medicaments i risc de pneumònia

Els analgèsics opiacis causen depressió respiratòria amb la hipoventilació pulmonar resultant;

alguns d’ells (codeïna, morfina, fentanil i metadona) també tenen efectes immunosupressors.

Incrementen el risc de pneumònia i la mortalitat respiratòria en un 40 a 75%.26,27,28

L’any 2018, uns 50 milions de persones als EUA (15% de la població adulta, 25% entre els més

grans de 65 anys) reberen una mitjana de 3,4 prescripcions d’analgèsics opiacis, i 10 milions de

persones reconeixien consum exagerat d’analgèsics de prescripció mèdica.29 A Europa en els

últims anys el consum d’opiacis suaus y forts ha augmentat, sobretot entre la gent gran.30,31

Fentanil i morfina son els opiacis forts més consumits, i més recentment oxicodona. El

tramadol, que és també inhibidor de la recaptació de serotonina, és l’opiaci suau més consumit.

En dos estudis observacionals de publicació recent, el consum de tramadol, comparat amb el

d’AINE, es va associar a una mortalitat 1,6 a 2,6 vegades més alta,32,33 sobretot en pacients

amb infecció i en pacients amb malaltia respiratòria.

17 de juny 2020

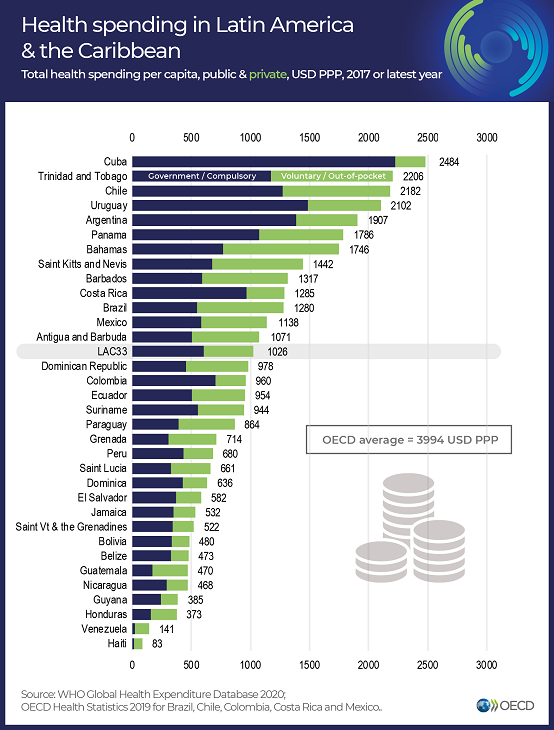

LATAM Health at a glance

Panorama de la Salud:Latinoamérica y el Caribe 2020

Health at a Glance: Latin America and the Caribbean 2020

This is a joint report by OECD and World Bank. It is a key reference to understand health in LATAM and Caribbean. You'll find:

Spain Health expenditure per capita 2.446 € , Cuba Health expenditure per capita 2.484 $ !!!

Health at a Glance: Latin America and the Caribbean 2020

This is a joint report by OECD and World Bank. It is a key reference to understand health in LATAM and Caribbean. You'll find:

Key indicators on health and health systems in 33 Latin America and the Caribbean countries. This first Health at a Glance publication to cover the Latin America and the Caribbean region was prepared jointly by OECD and the World Bank. Analysis is based on the latest comparable data across almost 100 indicators including equity, health status, determinants of health, health care resources and utilisation, health expenditure and financing, and quality of care. The editorial discusses the main challenges for the region brought by the COVID-19 pandemic, such as managing the outbreak as well as mobilising adequate resources and using them efficiently to ensure an effective response to the epidemic. An initial chapter summarises the comparative performance of countries before the crisis, followed by a special chapter about addressing wasteful health spending that is either ineffective or does not lead to improvement in health outcomes so that to direct saved resources where they are urgently needed.

Spain Health expenditure per capita 2.446 € , Cuba Health expenditure per capita 2.484 $ !!!

16 de juny 2020

Risk adjustment, a work in progress

Risk Adjustment, Risk Sharing and Premium Regulation in Health Insurance Markets: Theory and Practice

This is a handbook on an unfinished topic. Risk adjustment is required for any managed competition model to work properly (Enthoven model) and for any funding of plans that tries to promote efficiency and avoid selection:

This is a handbook on an unfinished topic. Risk adjustment is required for any managed competition model to work properly (Enthoven model) and for any funding of plans that tries to promote efficiency and avoid selection:

The Enthoven model has evolved as its ideas have been applied in particular institutional contexts. Today, sophisticated risk adjustment models give a regulator an effective tool to quantify differences among individuals in their expected healthcare costs. Rather than a system of risk-rated premiums, regulators rely more on risk adjustment to pay plans more for higher-risk enrollees. Also, the countries in which the regulated competition model has become dominant (e.g., Germany, the Netherlands) are characterized by separation of the functions of health insurance and healthcare provision. Regulated competition can and has been implemented without the presence of integrated HMO typeTherefore, any regulator interested in mitigating health insurance market failures should read it.

risk-bearing delivery systems. In these countries, and in other settings such as Medicare Advantage in the United States, regulated competition is oriented to the health insurers, not the healthcare delivery system.

Throughout this evolution, the key feature of Enthoven’s model remains: an active collective agent on the demand side of health insurance structures and manages the health plan market to overcome market failures. Enthoven calls this agent a “sponsor,” a role that can be fulfilled by various organizations. In health insurance markets today, sponsors are mainly governments (as is common in Europe and the United States) and employers (as is common in the United States). In this volume we will generally refer to a “regulator.”

Subscriure's a:

Missatges (Atom)