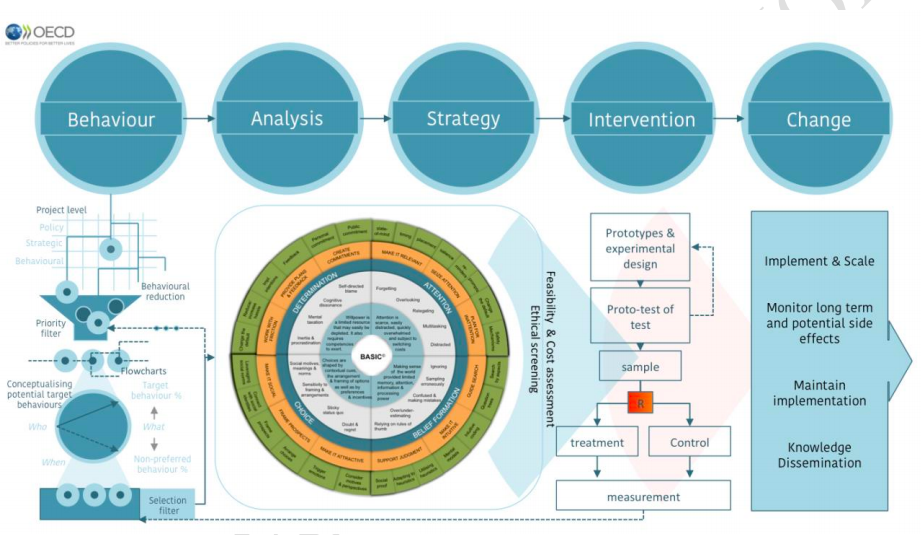

This OECD report is really helpful. It tries to provide a concret approach to behavioral insights for policy makers. It goes beyond standard nudging perspective.

A weekly conversation that looks at the way technology is changing our economies, societies and daily lives. Hosted by John Thornhill, innovation editor at the Financial Times.

Prescription drug sales for 2010 through 2018 grew at a CAGR of +2.3%. This can be compared to the forecast annual CAGR of +6.9% for 2019 through 2024 with expected sales to reach $1.18trn. The growth rate for the prescription market in 2019 is forecast to be +2.0%, which depicts a decline in growth rate compared to 2018 (+5.0%). So far the industry has seen a major set-back with one of the biggest failures, aducanumab, which was discontinued in Phase 3 trials for Alzheimer’s disease.Distrust fortune tellers. Nobody knows anything about the future.

Pricing health services is a key component in purchasing the benefits package (the covered services) within the overall financing system (Evetovits, 2019). Pricing and payment methods are important instruments in purchasing that provide incentives for health care providers to deliver quality care. A second instrument is contracting, in which the conditions for the payment of services are defined, and prices can be used as signals to providers. A third is performance monitoring. Where health care providers are rewarded based on the outcomes they achieve, these payments also must be priced correctly to provide the right incentives.Right, there are more elements in the equation than prices, but the tools for fine tunning are too open. Anyway, this report is really welcome and the cases are well described.

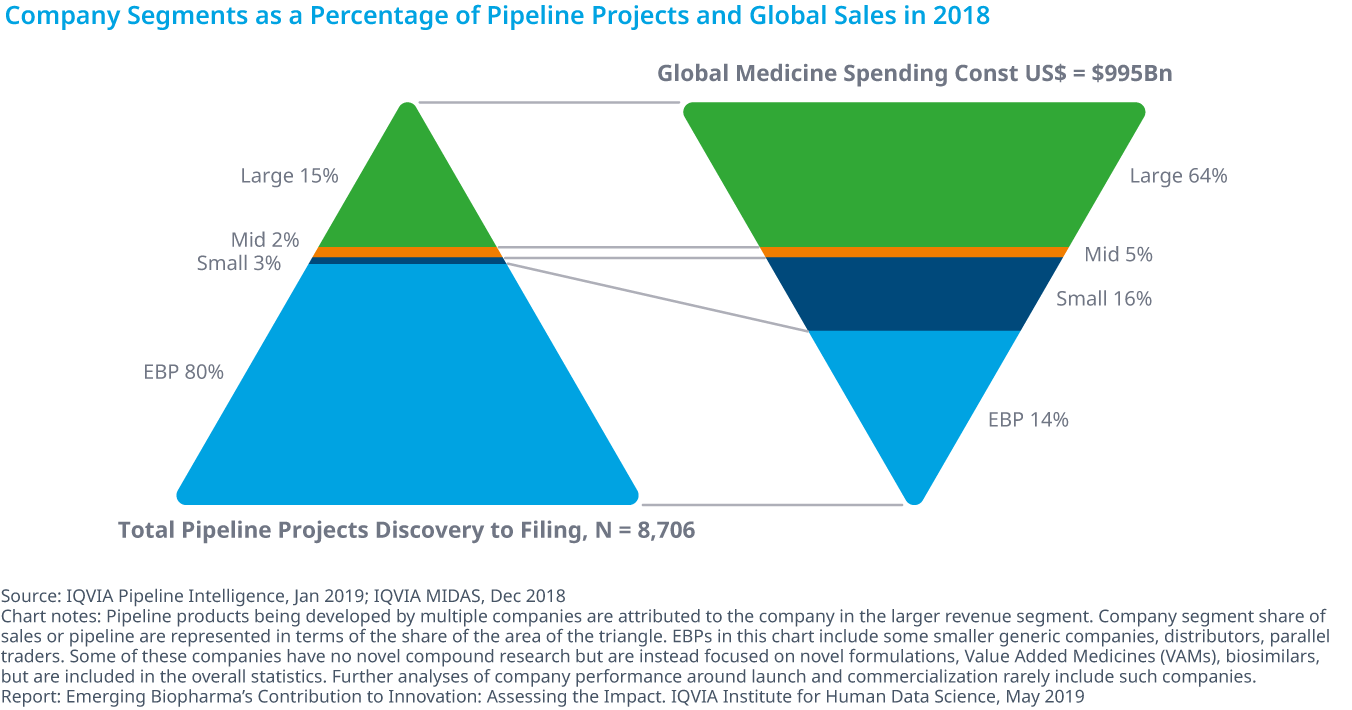

- Emerging biopharma companies accounted for 73% of the total late-stage R&D pipeline in 2018, compared with 61% in 2008.

- Large pharma companies have seen their share drop from 27% to 19% from 2017 to 2018.

- The share of mid-sized and small pharma companies developing novel products has remained steady since 2003, with small pharma developing approximately 5–6% of products and mid-sized pharma developing from 2–5%.

- Emerging biopharma companies are increasing their pipeline share, because they are the most active in the fastest-growing areas of oncology and orphan drugs, and because they increasingly can develop their innovations without the need to partner or be acquired.

The 2018 launch of 15 new active substances (NASs) bring the total NAS launches since 2013 to 57 with 89 approved indications for 23 different tumor types Within the R&D oncologic pipeline, the most intense activity is for immunotherapies, with almost 450 in clinical development A total of 1,170 oncology clinical trials were initiated in 2018, an increase of 27 percent from 2017 and 68 percent from 2013 More than 700 companies across the globe have oncology drugs in late-stage development, including 626 emerging biopharma companies and 28 out of the 33 largest pharma companiesOn costs in USA:

The average annual cost of new medicines continues to trend upward, although the median cost dropped $13,000 in 2018 to $149,000, and cost per product ranged betweenOn value?

$90,000 and over $300,000. The mean cost for new brands in 2018 was $175,578, down from $209,406 in 2017, but was above the $143,574 mean from 2012 to 2018.

Spending on cancer medicines is heavily concentrated, with the top 38 drugs accounting for 80% of total spending. Over half of cancer drugs earn more than $143.6 million in annual sales and in aggregate account for only 2.2% of oncology spending.

We find that the overall success rate for all drug development programs did decrease between 2005 (11.2%) and 2013 (5.2%), as anecdotal reports suggest. However, this decline reversed after 2013. The overall success rate is mainly driven by changes in POS1,2 and POS2,3. The timing of the upward trend coincides with the time period during which the FDA has been approving more novel drugs,compared to the historical mean.Quite surprising. The accelerated approval by FDA ends with more drugs withdrawn from the market. Therefore, the probability of success is a flawed statistic. It should be adjusted according to regulator criteria.

LTC needs are increasing rapidly and neither the market nor the family seem to be able to meet such a mounting demand. Furthermore, the existing public programs are both insufficient and uncoordinated. For these reasons we advocate developing a full-fledge LTC public insurance scheme that would fulfill two objectives: assisting those who cannot count on any family assistance and do not have the financial means of purchasing LTC services and providing the middle class a program that would protect families against too costly spendingIs there enough public money to pay for this?

Observational study on secondary data from virtually all hospital care episodes produced in 51integrated providers (i.e., administrative healthcare areas) and 67 hospitals, in 2003 and 2015. Alzira’s2015 performance (and its variation since 2003) was compared with all public-tenured peers in the SNHS,using 26 indicators analysing the differences in age-sex standardized rates of events or risk-adjusted mortality, severity-adjusted hospital expenditure and hospital technical efficiencyAnd the conclusion is:

In this comprehensive comparative study on Alzira’s performance, this PPP has not generally outperformed public-tenured providers, although in some areas of care its developments have been outstanding.I agree on the methodology, I can't asses the results and its conclusions because it requires data replication. What it is crucial is the clinical decision making within the health organization (the microsystem and its episodes of care), forget generalizations on public and private and focus on drivers for efficiency in each setting.